The global tanker fleet is getting older—and fast. As of 2025, 22% of tankers are over 20 years old, and nearly half of the fleet will surpass 21 years by 2030. This ageing trend poses safety, efficiency, and compliance risks, especially as IMO 2030 and 2050 decarbonization targets tighten.

Yet, renewing the ageing Tanker fleet is far from straightforward. Owners face low freight rates, weak scrap values, and shipyard bottlenecks, all while navigating uncertainty over future fuel technologies.

The Ageing Tanker Problem

Average Age Rising: The global tanker fleet’s average age has climbed above 14 years, up from 10 years in 2018.

Operational Risks: Older vessels suffer from higher maintenance costs, lower fuel efficiency, and greater downtime.

Regulatory Pressure: IMO rules demand double hulls, advanced emissions controls, and energy efficiency measures, making older ships increasingly non-compliant.

Shipyard Capacity Constraints: A Bottleneck for Renewal

Even if owners want to order new tankers, shipyard slots are scarce:

Delivery Times Extended: Lead times for VLCCs have stretched from 2 years to 3+ years, with the earliest slots often unavailable before 2028.

Competition for Berths: LNG carriers, container ships, and offshore units compete for the same berths.

Global Capacity Shrinkage: Shipyard capacity has fallen 40% since 2009, and labor shortages further constrain output.

Low Freight Rates and Scrap Values: Why Owners Hesitate

Freight Market Weakness: Tanker earnings have softened after the post-pandemic boom.

Scrap Values Depressed: Recycling prices have failed to incentivize demolition, leaving older ships trading longer.

Orderbook Collapse: Product tanker newbuild contracting dropped 86% year-on-year in 2025, hitting a nine-year low.

Economic Equation for Owners

High Newbuild Prices: Tanker newbuilding costs remain elevated due to steel prices, labor shortages, and inflation.

Uncertain Payback: Low freight rates and unclear future fuel regulations make ROI on newbuilds risky.

Secondhand Market Dynamics: Older ships still fetch strong prices in sanctioned trades, reducing scrapping incentives.

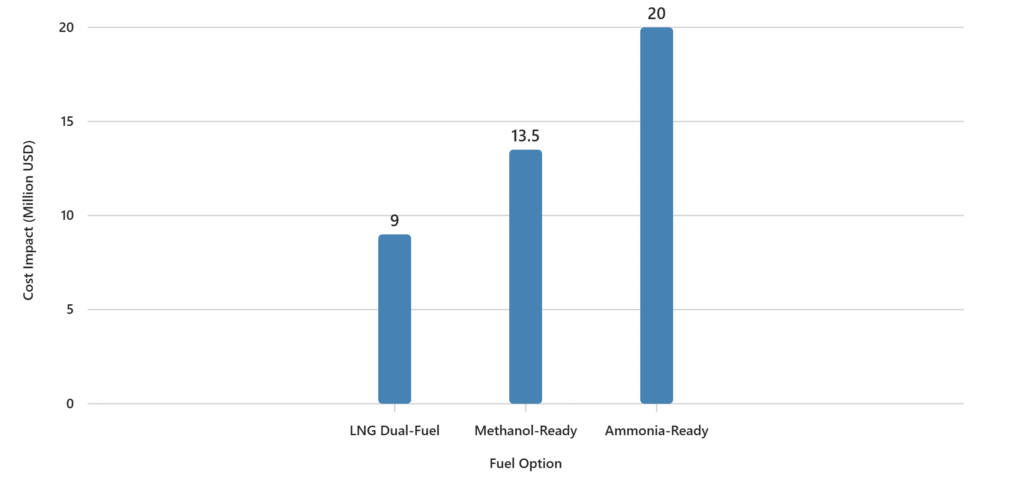

Alternative Fuel Engines: Choices and Costs

Decarbonization adds another layer of complexity. Owners must decide whether to:

Option 1: LNG Dual-Fuel

Pros: Mature technology, lower CO₂ emissions.

Cons: Methane slip concerns, infrastructure gaps.

Cost Impact: Adds \$8–10 million to VLCC newbuild price.

Option 2: Methanol-Ready

Pros: Liquid at ambient temperature, easier storage.

Cons: Lower energy density, higher fuel cost.

Cost Impact: Retrofit-ready design adds \$3–5 million upfront; full methanol dual-fuel adds \$12–15 million.

Option 3: Ammonia-Ready

Pros: Zero carbon emissions.

Cons: Toxicity, safety protocols, and large storage requirements.

Professional maritime news and technical analysis curated by a board of industry veterans with over 100 years of combined experience in Marine Engineering and Naval Architecture.