Introduction

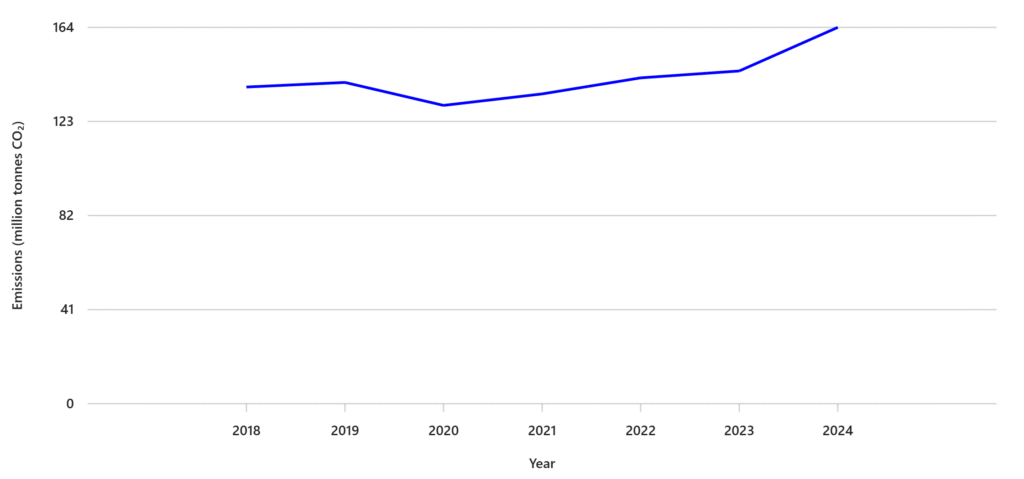

European shipping emissions reached their highest level since mandatory reporting began in 2018, marking a 13% increase in 2024 despite a slowdown in trade volumes. This paradox highlights the complexity of maritime decarbonisation and the urgent need for robust policy interventions. According to the EU’s Monitoring, Reporting and Verification (MRV) system, container ships were the primary culprits, with emissions soaring by 46% due to longer routes and higher operational speeds caused by geopolitical disruptions in the Red Sea.

Drivers Behind the Emissions Spike

- Geopolitical Disruptions

The Houthi attacks in the Red Sea forced vessels to reroute around the Cape of Good Hope, increasing sailing distances by 18% and operational speeds by 3%. Each 1% increase in speed can raise emissions by up to 3%, making operational adjustments a critical factor in emissions growth. - Container Shipping Dominance

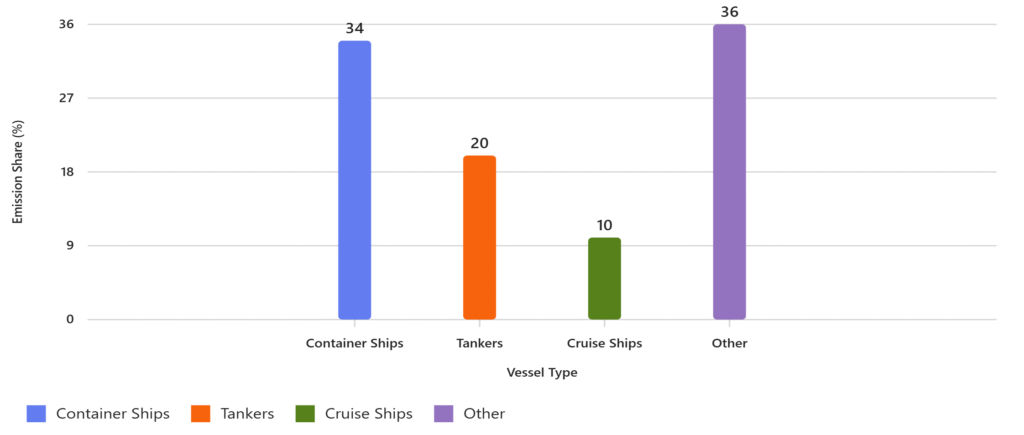

Container ships accounted for 34% of total emissions under the EU ETS scope, despite representing only 16% of vessels. Their operational pressures—longer routes and tight delivery schedules—led to disproportionate emissions compared to other vessel types. - Persistent Fossil Fuel Transport

Fossil fuel carriers remain responsible for 20% of EU shipping emissions, unchanged since 2018. While LNG-related emissions declined slightly in 2024, crude oil transport emissions rebounded to 2019 highs, underscoring Europe’s continued reliance on fossil fuels.

Regulatory Landscape: ETS and FuelEU Maritime

- EU Emissions Trading System (ETS)

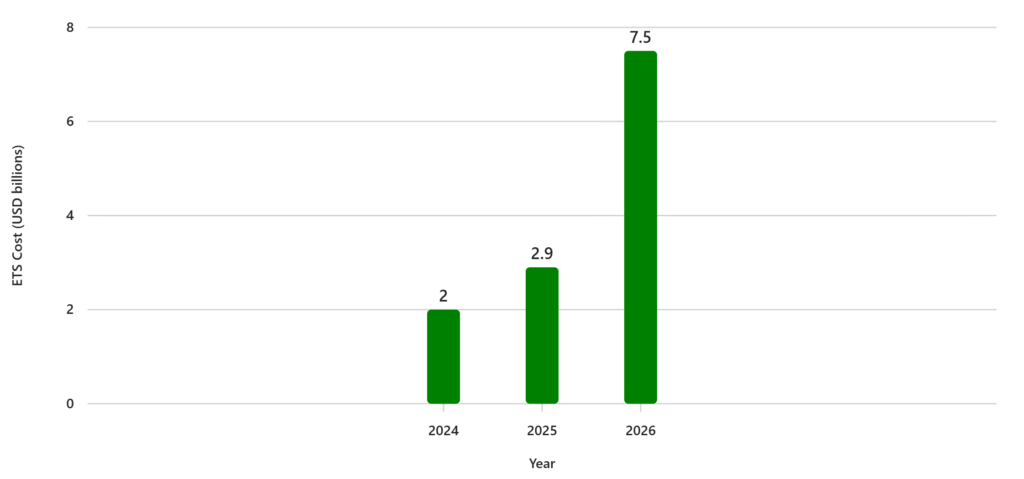

Shipping entered the ETS in 2024, requiring operators to surrender allowances for 40% of their emissions, rising to 100% by 2026. Compliance has been strong, with 99% adherence in the first year. Financially, the sector faces significant costs—estimated at USD 2.9 billion in 2025, potentially rising to USD 7.5 billion by 2026. - FuelEU Maritime Regulation

Effective from January 2025, FuelEU mandates progressive reductions in the greenhouse gas intensity of marine fuels—2% by 2025, 6% by 2030, and 80% by 2050. It applies to all ships above 5,000 GT calling at EU ports and covers CO₂, methane, and nitrous oxide on a well-to-wake basis. This regulation complements ETS by incentivising the uptake of renewable fuels such as e-methanol, ammonia, and hydrogen.

Industry Response and Challenges

- Green Fuel Adoption

Despite regulatory pressure, the transition to alternative fuels remains slow. Biofuels and LNG are gaining traction, but RFNBOs (Renewable Fuels of Non-Biological Origin) are still in early stages due to cost and infrastructure constraints. [ - Operational Efficiency

Measures like slow steaming, hull optimisation, and advanced antifouling coatings are being deployed to reduce fuel consumption. However, these steps alone cannot offset the emissions surge caused by longer routes and higher speeds.

Decarbonisation Trends and Future Outlook

The EU’s Fit for 55 package and Horizon Europe investments signal a strong commitment to zero-emission shipping by 2050. Yet experts warn that without accelerated innovation and stricter enforcement, emissions could continue to rise, jeopardising climate targets. Eliminating fossil fuel dependency would cut 20% of emissions, but over 80% still require decarbonisation through efficiency gains and green hydrogen-based fuels.

Key Takeaways

- Record High Emissions: 13% increase in 2024 despite reduced trade.

- Main Culprit: Container ships (+46% emissions).

- Regulatory Push: ETS and FuelEU Maritime aim to curb emissions.

- Persistent Challenge: Fossil fuel transport accounts for 20% of emissions.

- Future Path: Green fuels, operational efficiency, and global alignment are critical.